Solar power is set for explosive growth in India, matching coal’s share in the Indian power generation mix within two decades or even sooner in the Sustainable Development Scenario.

This was mentioned in the recently released India Energy Outlook 2021 report by IEA which explores the opportunities and challenges ahead for India as it seeks to ensure reliable, affordable and sustainable energy to a growing population. The report examines pathways out of the crisis that emerged from the Covid-19 pandemic, as well as longer-term trends, exploring how India’s energy sector might evolve to 2040 under a range of scenarios.

India has seen extraordinary successes in its recent energy development, but many challenges remain, and the Covid-19 pandemic has been a major disruption.

India is the world’s third-largest energy-consuming country, thanks to rising incomes and improving standards of living. Energy use has doubled since 2000, with 80% of demand still being met by coal, oil and solid biomass. On a per-capita basis, India’s energy use and emissions are less than half the world average, as are other key indicators such as vehicle ownership, steel and cement output.

The report focuses on the Stated Policies Scenario (STEPS) provides a balanced assessment of the direction in which India’s energy system is heading, based on today’s policy settings and constraints and an assumption that the spread of Covid-19 is largely brought under control in 2021.

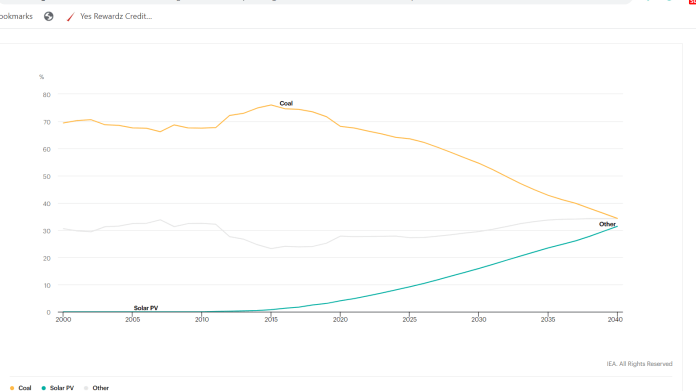

As things stand, solar accounts for less than 4% of India’s electricity generation, and coal close to 70%.

By 2040, they converge in the low 30%s in the STEPS, and this switch is even more rapid in other scenarios. This dramatic turnaround is driven by India’s policy ambitions, notably the target to reach 450 GW of renewable capacity by 2030, and the extraordinary cost-competitiveness of solar, which out-competes existing coal-fired power by 2030 even when paired with battery storage.

The rise of utility-scale renewable projects is underpinned by some innovative regulatory approaches that encourage pairing solar with other generation technologies, and with storage, to offer “round the clock” supply. Keeping up momentum behind investments in renewables also means tackling risks relating to delayed payments to generators, land acquisition, and regulatory and contract uncertainty.

However, the projections in the STEPS do not come close to exhausting the scope for solar to meet India’s energy needs, especially for other applications such as rooftop solar, solar thermal heating, and water pumps.

Discover more from SolarQuarter

Subscribe to get the latest posts sent to your email.

{kind=link}