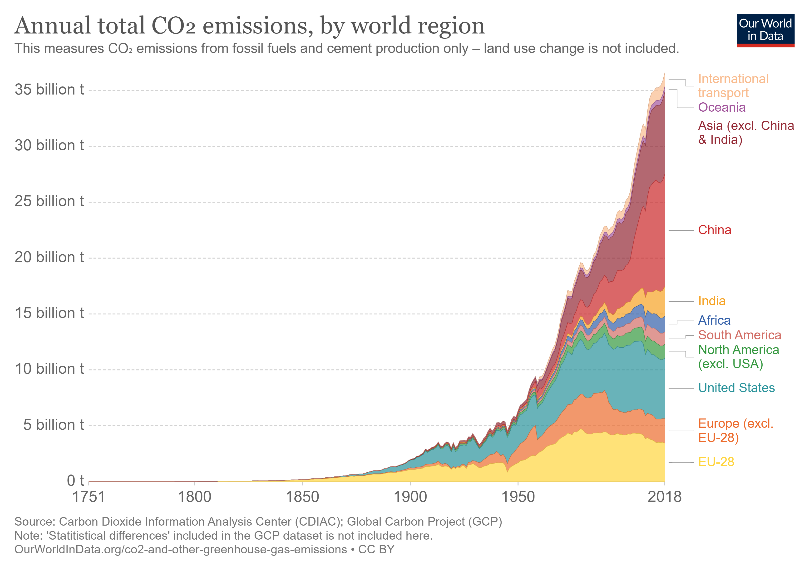

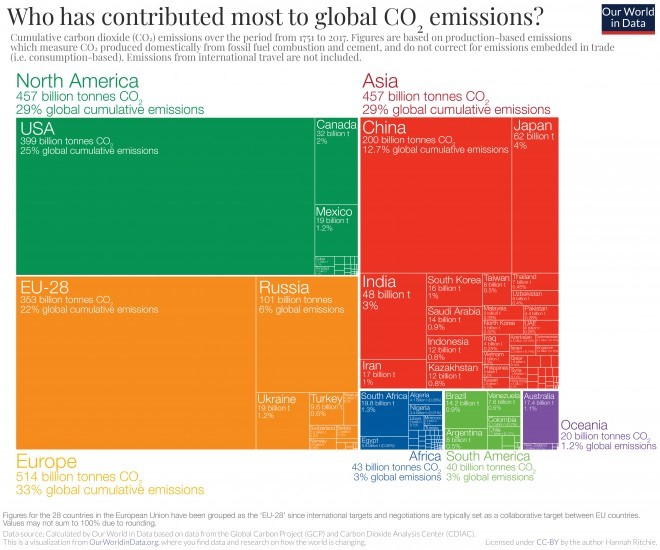

Since 2015 India has seen an economic growth of 6.7% per year on average and has successfully improved the life of hundreds of millions of citizens. Historically, India has only contributed to 3% of the cumulative emissions since the XVIII century. But as emissions from OECD countries are decreasing, several emerging markets see their emissions growing at a fast rate, and among them India is one of the most important.

Catching up with the HDI level of mature economies, while trying to control its emissions, and more generally trying to limit the environmental impact of its growth, India has to face many challenges at the same time. The good news is that there are already many technologies available to help the country, as well as international investors ready to partner with Indian consortium and bring additional funding to the table.

An Incredible Trajectory

An outstanding result of recent policies is the connection of 50 million additional people – the equivalent of the Spanish population getting access to electricity – every year since 2015. Over 90% of the population now has access to basic water service.

As the population becomes more urban, there is a fast increase in use of appliances and modern cooking. The growth of the construction industry, to increase the number of buildings and city infrastructures, is therefore massive, with materials such as plastic, cement, steel, aluminum and chemicals.

The country has now the second largest in the world road network. And the fourth largest railway network, of which 50% is already electrified, with a target to have 100% of the electricity consumption equivalent being covered by renewables.

India has also put a strong emphasis on energy efficiency, in all segments of the economy. A good example is the LED program launched in 2015, the “Unnat Jyoti by Affordable LEDs for All” (UJALA) which has contributed to generate more than 54TWh/y of savings.

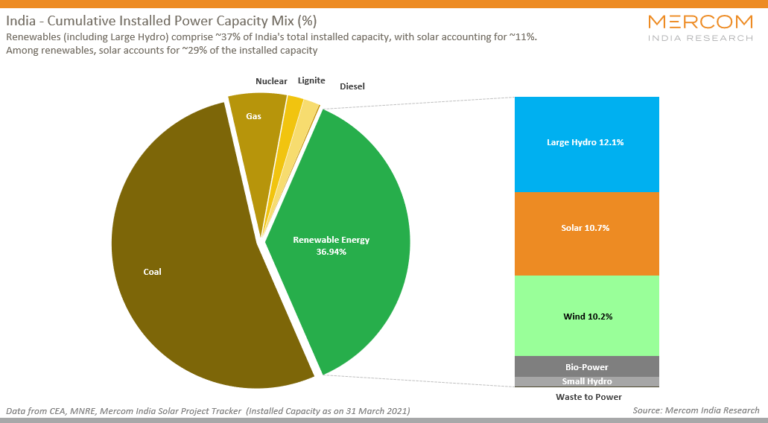

In the power sector, a most noticeable feat has been the development of renewable energy, which now provides 7% of the total generation, twice the share as in 2014. The average growth rate for solar has been 60% and 10% for wind, compared to 7% in overall installed capacity. Today installed solar capacity is slightly above 40GW and 39 GW for wind.

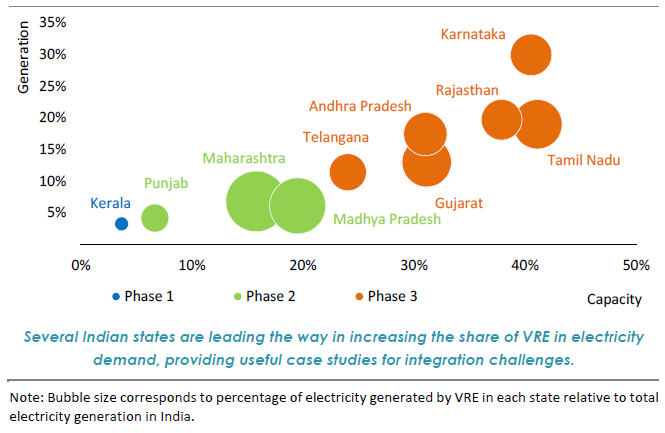

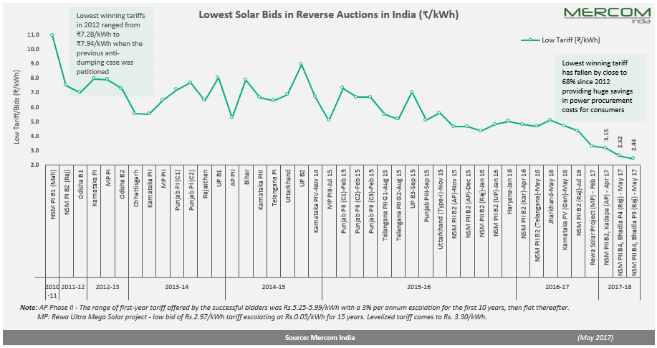

Some regions have a share of variable renewable (VRE) above 20% or even 30%. Average bid prices have steadily decreased over the past 10 years: from 8.77rps/kWh in 2011, PPA tariffs have now reached tariffs as low as 2.36rps in 2020, which means a decrease of more than 73%.

With Many Challenges Ahead

Despite these successful outcomes, challenges ahead are still many. Pollution in cities has reached extraordinarily high levels. Cooking still relies on traditional biomass and is responsible for close to 800,000 premature deaths in 2019.

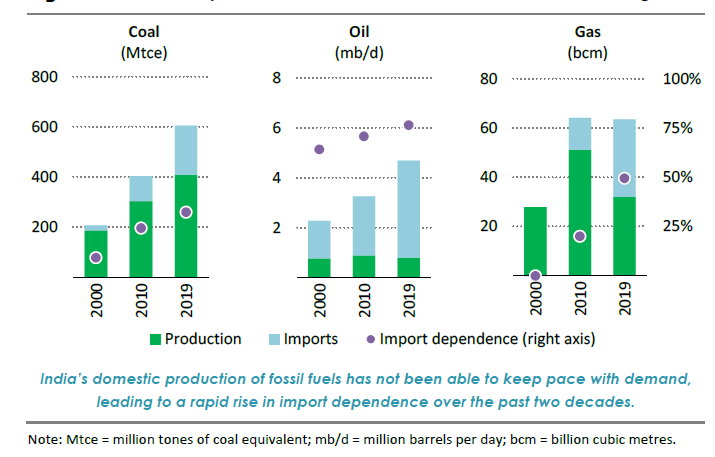

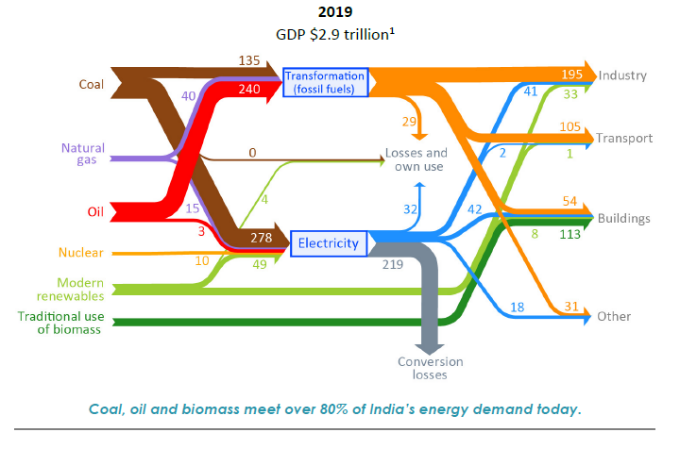

Oil consumption has never been that high, and renewables have not been able to replace coal, whose use is still growing, especially in the industry. Coal remains 44% of the primary energy used in India, followed by oil and biomass. In fact, India has installed more coal-fired plants than renewable during the period 2015-1019 (58GW vs 49GW). Coal only uses half of the railway capacity available for commodity transport.

India is facing incredible challenges in keeping pace to supply the necessary infrastructure for its growing population which is becoming more urban with access to basic infrastructure: in the past three decades, the transport sector has increased fivefold, leading to pollution, road congestion and higher dependency on oil, on which it relies at 95%. About 75,000 vehicles per day of all types are sold. And 2/3 of the buildings which will exist in 2040 in India, have yet to be constructed. This shows the massive growth of industries and services, and all associated activities which will be important drivers for the energy demand in India.

The development of renewables, although spectacular, has been way below the initial targets announced in 2015 of 175GW by 2022 (vs 80GW in 2021). There are numerous reasons for that, among them:

- Difficulties in land acquisition

- Financial difficulties of distribution company

- Existing contracts with fossil fuel IPP

- Learning curve of the sector: initial bids became quickly very aggressive, making projects implementation more difficult, while now players have been able to get organized, and play a healthier competition

What’s next? India and the Energy Transition

I would like to discuss 3 elements in this section:

- Selected energy scenarios to identify some common features

- As solar and wind will play a key role in the future energy system of India, selected actions to contribute to their expansion

- Impact of GDP growth on the environment

- Different energy scenarios, different futures

There are numerous scenarios which have been built in the past years, and certainly more will come in the future, as technologies and regulations evolve.

The IEA scenarios

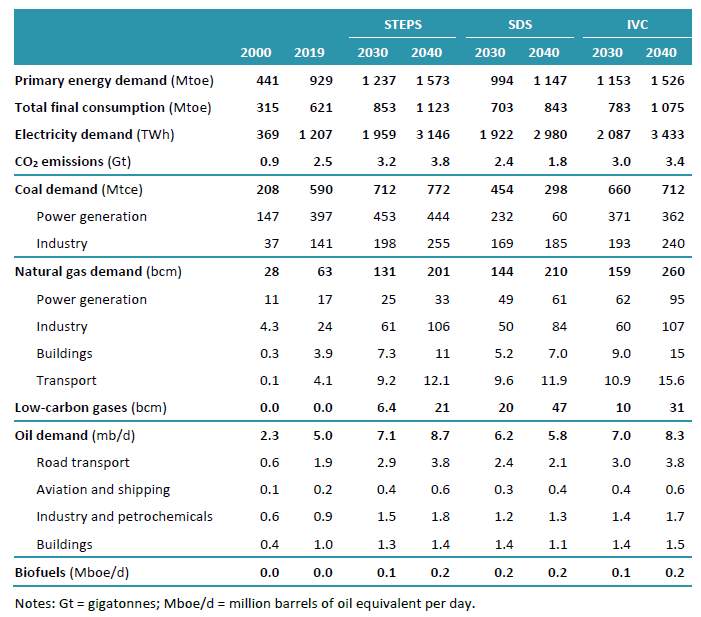

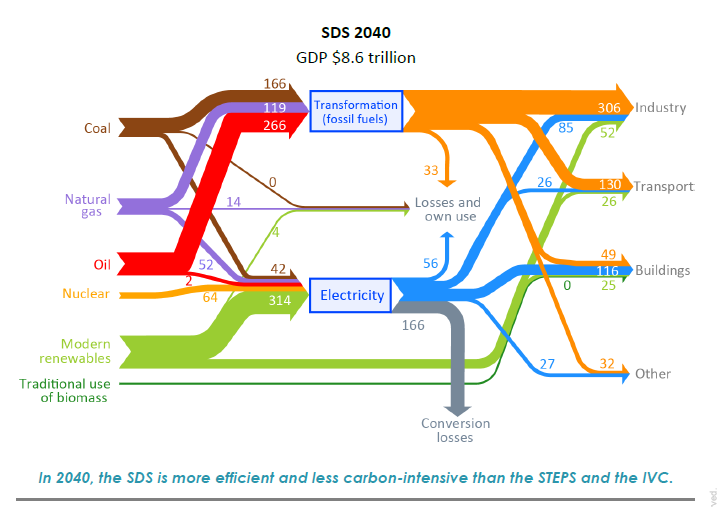

The IEA has proposed 3 different scenarios: STEPS/SDS/IVC. IVC takes an optimistic view that all political announcements and targets are met, but national and international. STEPS is a more pessimistic/realistic view concerning these commitments. SDS takes a different approach: it’s a scenario based on achieving certain environmental targets (UN SDGs for example) and see the milestones that need to be achieved backwards.

There are few remarks which can be drawn from these scenarios:

- Coal demand for the power sector can longer increase. And it has to decrease significantly if India has to achieve its environmental targets, while increase in coal demand for the industry should be kept at its bare minimum. These two elements, by themselves, have very strong implications for the Indian economy and imply a complete set of actions and regulations, across different sectors

- In all scenarios, by 2040, the electricity demand will be x3, and solar capacities are supposed to be at least x20 by 2040, while wind will be almost x8. At least 150GW of batteries will be installed

- Gas will play an increasing role in the industry

100% RE scenario

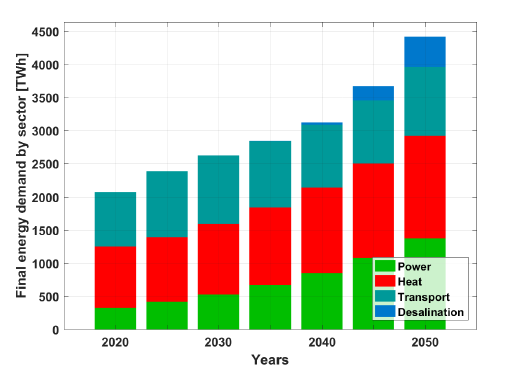

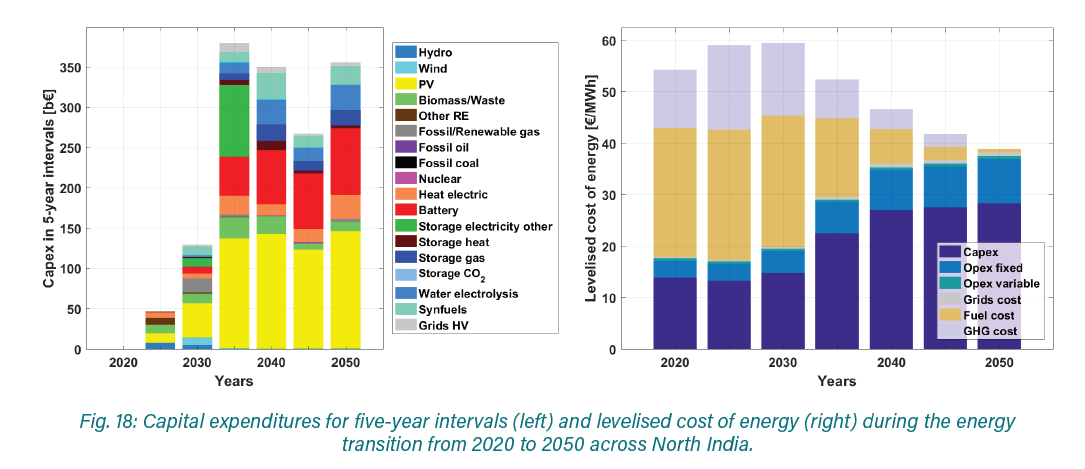

Another interesting scenario was proposed by Climate Trends (India) and LUT University (Finland). They have simulated a 100% RE scenario for Northern India. The map below shows the interconnections and exchanges between states, the evolution of the final energy demand and the CAPEX planned, as well as the LCOE of the system achieved.

It shows that by 2050 it is feasible to achieve such a system, with a very competitive LCOE. The technological deployment is massive, and solely focused on clean energy. It gives an idea of the investment amount at stake:

The total annual system costs increase from around 120 bUSD in 2020 to over 190 bUSD in 2050. These amounts cover all major sectors: power, heat and transport. Capital costs are well spread across a range of technologies with major investments for solar PV, batteries, heat pumps, and synthetic fuel conversion up to 2050. A majority of the investments are in the later periods of the transition from 2035 onward, as the energy system requires more flexibility solutions with higher shares of renewables

Fuel imports and the respective negative impacts on trade balances will fade out through the transition, as e-fuel starts to be produced by 2045, leading to great energy security

System LCOE can reach a cost as low as 41USD/MWh by 2050 and is increasingly dominated by capital costs as fuel costs continue to decline through the transition period, which could mean increased self-reliance in terms of energy for North India by 2050.

More Renewable, Faster, Cheaper

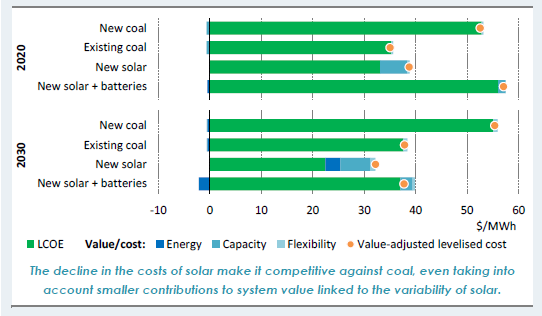

As electrification will play a key role in the decarbonation of the Indian economy, the development of renewable energy is of utmost importance. These technologies have the potential to positively disrupt emission trends, fossil uses as well as the social, economic and technological environments in India.

As they continue to develop, they will become cheaper and cheaper, making them the number 1 choice in all investment decisions, and allowing them to be integrated in all sectors, in particular transport and industry. Their development also drives innovation and industrial policies and therefore the regulatory environment should provide a whole integrated approach.

It is key that these technologies reach a point when they become naturally the cheapest option. This situation is very near to happen in India, as new coal projects are above 55USD/MWh, existing between 35-40USD/MWh, and solar + batteries around 40USD/MWh.

IRENA Coalition for Action, in which Dii Desert Energy is an active member, has recently published a white paper suggesting a few key drivers for the current decade.

I will quote some of the key elements below:

- Accelerate the coal phase out

- The government may consider an ambitious timeline for coal phaseout while putting in place adequate policy to ensure a just transition for regions and populations relying on the coal economy.

- Removing subsidies for coal will enable substantial public savings that could be channeled into additional investment in energy transition-related technologies and infrastructure

- Ensure long-term policy certainty, clarity on permitting and consenting for renewable energy projects and predictable and transparent tendering process

- The main areas of concern of investors today are delayed/cancelled tendering schemes, renegotiated power purchase agreements (PPAs), delayed payments, delayed grid connectivity and retrospective changes in land acquisition. In the wind sector, changes in land policies have impacted the timelines and costs of many projects awarded under central auctions.

- A clear and long-term schedule/trajectory for upcoming auctions would allow developers to better plan their participation, adjust their expectations and quote sustainable tariffs in their proposals

- There is also a need for a clear definition of all sector coupling policies, such as heating and cooling and transport

- Upgrade the capacity of transmission and distribution systems

- The lack of short and long-term grid visibility has been a growing concern for the renewable energy industry and sometimes is cited as a reason for low participation in auctions. In some regions, land availability and high resource potential sites around substations have resulted in grid congestion. Planning timelines for grid connection outpace plans for grid augmentation, resulting in delayed projects.

- Grid augmentation and construction of additional substations should be prioritized to ensure that renewable energy can be widely integrated across the country. In the process of grid modernization, the government may also opt to implement technical improvements for forecasting and smart distribution systems, to support balancing with a larger share of renewable energy.

- Strengthen policy frameworks for storage and system flexibility solutions

- The Indian government has stated the need for an additional 35 GW of storage capacity by 2030 to support the transition, up from just under 5 GW today. To realize this ambition, a comprehensive regulatory framework should be adopted that provides investors with clear price signals, including through the provision of appropriately remunerated ancillary services.

- 24/7 Renewables+storage tenders, involving both pumped storage and battery energy storage, are another positive step to improve renewable energy integration. Further round-the-clock tenders can incentivize the development of hybrid projects by strengthening the requirements for even dispatch on a scheduled basis.

New Development Schemes

The social and energy transformation of India is under way. In all scenarios, renewable and electrification will play a leading role in providing both the fuel for its economic development and decorrelate emissions for GDP growth. Still, even in the most optimistic scenario of the IEA, GDP in 2040 is four times the GDP in 2019.

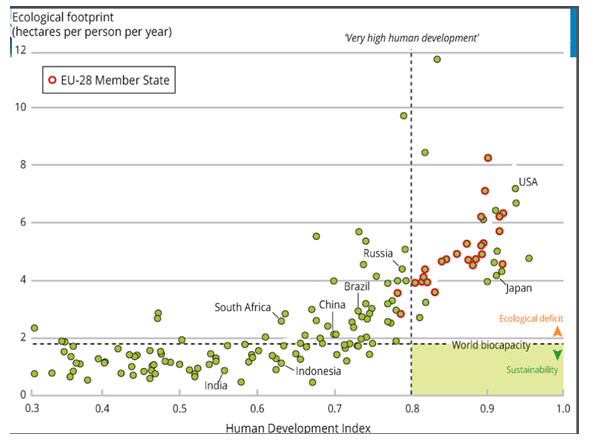

Massive industrial development, infrastructure (road, buildings), material consumption are required to reach this stage. Decarbonizing its economy in the coming three decades, while improving its HDI and managing its population growth of 1.3% per year – expected to peak close to 2050 – represent an incredible challenge. If India is set to follow the same path of more mature economies, then increasing its IDH will come in conjunction with an increase of its ecological footprint, as shown in the graph.

Finding new social models, where growth would have a different significance, would alleviate the environmental pressure which will be exercised, but also alleviate the financial burden on the economy. These strategies could rely on 3 main pillars:

- technology – such as new construction material

- regulation – such as carbon tax, with redistribution schemes

- infrastructure – such as new urban planning to decrease use of vehicle and organize space differently

Conclusion

All eyes have been on India during the past decade, and the country has been internationally acknowledged as a successful example of an innovative and ambitious policy in developing renewable energy. India is home of the International Solar Alliance, which is supporting a worldwide development of solar and backing several initiatives in emerging markets. Large successful renewable energy platforms have been created, in joint ventures between international players, such as energy companies, private investment funds or pension funds, and local industrial groups. A large portion of the value chain is located in India, with some companies belonging to Tier 1 groups. Project finance is well developed, and the size of the market is attractive.

When looking at the challenging ahead, India could in the future also capitalize on this success, and develop new types of international collaboration, be it technical or financial, not only to strengthen the development of renewable energy, but also to develop other sectors such as construction, urban planning, transport, and provide attractive frameworks to foster these collaborations.

By Karim Megherbi, Executive Director, EPDA

Discover more from SolarQuarter

Subscribe to get the latest posts sent to your email.

{kind=link}