India’s installed renewable energy output capacity has increased at a rapid pace, achieving a CAGR of 17.33% between FY16-20. With the government’s increased emphasis on the growth of the renewable energy sector, India’s solar photovoltaic industry has already taken off in order to meet the aim of 100 GW of solar power generating capability by 2022.

Numerous government subsidies and incentives have raised understanding and sensitivity among end-users of solar power as an alternative source of energy to existing mainstream sources. So far, the Southern area of India has dominated major solar projects. However, as we approach 2022, current innovations and initiatives in the pipeline anticipate that the Northern area will outshine the Southern region in terms of maximum deployed solar PV capacity.

Given the ease of land acquisition and other legal permits from the federal and state governments, gigantic solar power plants are in full gear, with a tremendous amount of domestic and international investment flowing into the industry. The Indian government has also created a National Green Corridor Program to allow renewable power to stream into the national grid network.

With expanding scope and research on p-type and n-type monocrystalline silicon modules, standard and advanced Multicrystalline module technology have the biggest share in the shift. The capacity utilization factor of solar plants has improved as the cell efficiency of such sophisticated photovoltaic (PV) modules has increased.

Net-Metering, Accelerated Depreciation Mechanism, Feed-In Tariff, Generation Based Incentives, and other technological advancements in rooftop solar PV facilities have prompted the use of sustainable and renewable solar energy on a micro level, which is anticipated to escalate the solar rooftop PV market over the forecast period. It will also help the government comprehend its ambition of lighting every home in the country.

Solar PV systems are now among the most cost-competitive energy alternatives on the marketplace, thanks to an 85% cost reduction over the last decade. As it stretches its competitive strength, the solar sector will almost certainly increase its attempts to investigate novel configurations and business models.

In 2022, the sector may witness an increase in solar-plus-storage infrastructure projects, the exploration of floating solar PV modules, and the expansion of community solar projects into new markets.

Combining storage and solar provides cost savings, operational efficiency, and the ability to lower storage capital costs through the solar investment tax credit.

Thus, the year ahead promises fresh development avenues for the solar business, which might be boosted by climate-change-fighting initiatives from the government. However, certain issues remain. It will be fascinating to watch how new technology, business models, legislation, and investments will assist in addressing these problems and accelerating development in our solar energy sector projection for 2022.

Let read what our experts have to say about the “India Solar Energy Market Outlook 2022”

By 2022 India is set to install 175 GW of renewable energy capacity, which includes 100 GW from solar, 60 GW from wind, 10 GW from bio-power and 5 GW from small hydropower. Towards this goal, several government-led schemes have been launched for the promotion and development of renewable energy and it is quite evident that solar energy is the likely answer to India’s energy future requirements.

Where are we now?

Solar energy has taken a central place in India’s National Action Plan on Climate Change with the National Solar Mission (NSM) as one of the key Missions. The Mission’s objective is to establish India as a global leader in solar energy by creating the policy conditions for solar technology diffusion across the country as quickly as possible. Launched in 2010, the mission is a major initiative of the Government of India with active participation from States to promote ecological sustainable growth while addressing India’s energy security challenges. It also constitutes a major contribution by India to the global effort to meet the challenges of climate change.

The share of solar and wind in India’s 10 renewable-rich states — Tamil Nadu, Karnataka, Gujarat, Rajasthan, Andhra Pradesh, Maharashtra, Madhya Pradesh, Telangana, Punjab and Kerala — is significantly higher than the national average of 8.2 per cent.

The National Institute of Solar Energy has assessed the country’s solar potential to be about 748 GW, assuming 3% of the waste land area to be covered by Solar PV modules. Recently, India achieved 5th global position in solar power deployment by surpassing Italy. To encourage rooftop solar (RTS) throughout the country, notably in rural regions, the Ministry of New and Renewable Energy plans to undertake Rooftop Solar Programme Phase II, which aims to install RTS capacity of 4,000 MW in the residential sector by 2022 with a provision of subsidy.

What can we expect in 2022?

Recent trends underlying the main renewables integration challenges include the increasing variability of hourly demand, the need to ramp up requirements due to the impact of solar on net demand, short-term frequency variations, and local voltage issues. More sectors in India will consider solar power as their sustainable source of energy supply. This has been largely possible because of solar panel manufacturers, who spend considerable resources manufacturing solar panels and related components ingeniously, without relying on their Chinese counterparts. India’s dependence on Chinese solar energy products was a huge hindrance in effectively pricing components like wind turbines and panels.

Going forward, we will see more use of solar power, not merely for the commercial and residential sectors but also households. The access to solar power resources is expanding and likely to improve.

Challenges and the solution

The most important challenge for further scaling up renewables in India is the poor financial condition of power distribution companies (discoms), most of which are owned by state governments. Almost all renewable energy is purchased by such discoms, resulting in very long and unsustainable payment cycles. The renewable energy sector can continue to grow significantly and play a key role in India’s and the world’s ambition in tackling climate change.

It is important to build a strong grid infrastructure. This could be accomplished through financial incentives and technological advancements. Promoting and supporting solar cells, modules, and other hardware manufacturing units, modernising grid networks, incentivizing R&D efforts, and other infrastructure-related measures should also be considered.

Manoj Gupta, VP-Solar and Waste to Energy Business, Fortum India Pvt Ltd

——————————————

“Despite the adversities from last year, the sector displayed resilience and quickly bounced back so much that this year might prove to be the best year for renewables in India, especially solar. The sector has achieved significant milestones in 2021 such as reaching 100+GW of renewable installed capacity with solar dominating the mix, increase in investments by almost 50% quarter on quarter (Source: Mercom), and favorable government policies such as Introduction of Production Linked Incentive (PLI) schemes to promote domestic manufacturing, 100% FDI using the direct route, the launch of Green Hydrogen Mission and Green Term Ahead Markets to boost RE sales through exchange among others.

Having said that, the sector has also faced market challenges such as supply constraints, project costs increases triggered by an increase in raw material prices, freight charges, or the recent increase in module prices in addition to policy uncertainties or frequent changes in policies. To add to the woes of the project developers, the government has also notified BCD and other taxes which will additionally burden developers and inflate project costs. However, we still hope that the sector is able to tide over these issues constraining its growth, and 2022 proves to be a stronger year for renewables in India.”

Shriprakash Rai, Head – C&I Business, Amp Energy India

——————————————

“Installed solar power capacity in India has seen phenomenal growth over the past few years, claiming a CAGR of 17+% between FY 2014-FY 2020. While utility-scale and mega solar projects continue to be dominant contributors, the increase in India’s residential solar market has helped us advance in being amongst the top 5 countries globally, regarding solar installed capacity. Robust demand, better policy support, and increased awareness are significant growth drivers in residential solar adoption amongst independent homeowners. However, despite increased demand, these growth drivers depend heavily upon quality solution providers and policy support at local DISCOM level.

India’s residential solar market is expected to grow at a CAGR of 15+% for the next five years. This is aided by MNRE’s focus on providing subsidies to consumers for solar adoption. In July 2021, to encourage rooftop solar (RTS) throughout the country, notably in rural regions, the Ministry of New and Renewable Energy planned to undertake Rooftop Solar Programme Phase II, which aims to install an RTS capacity of 4,000 MW in the residential sector by 2022 with subsidy provision.

Several states such as UP, Maharashtra, Punjab, Haryana, AP, and Telangana announced subsidies of up to 40% for systems up to 3 KW capacity and 20% for 3-10 KW range. Though it seems lucrative, due to the almost single-minded focus on price in the competitive bidding process, there is a real risk of poor quality systems getting installed. The plant may just perform for as less as five to seven years, compared to its expected life of 25 years. Poor experiences seriously dampen the enthusiasm for adopting solar among consumers.

In terms of technology and innovation, since COVID-19, technology and digitization have become the cornerstone of renewable energy adoption. Efficiency in monitoring solar generation via mobile apps positively acts as a stepping-stone in building a smart home ecosystem, enabling energy storage and efficiency. Solar solutions are increasingly becoming aesthetically appealing, along with using elevated solar mounting structures to ensure that the rooftop space remains available to the consumer.

With increasing digitization, the future of solar would be enabled by distributed energy hubs producing and storing clean energy as per the demand pattern of the home, all at a click away on the consumer’s smartphone”.

Shaili Yadav, Business Head – HomeScape by Amplus Solar

——————————————

At the recently concluded 26th session of the Conference of the Parties (COP26) in Glasgow, India announced that it will raise its non-fossil energy capacity to 500 GW by 2030. Solar energy will play a key role in achieving this target.

As of November 2021, the nation has cumulatively added 48.56 GW of solar power capacity. From January to November this year, 11.1 GW of solar capacity has been commissioned across the country, which is 250% higher than the figures last year.

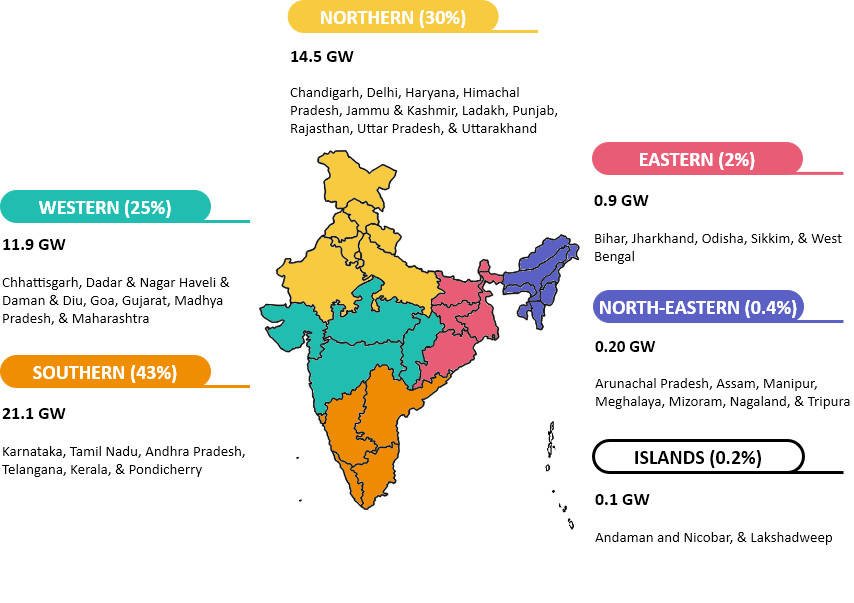

The southern region holds the highest share of 43%, followed by northern (30%), western (25%), eastern (2%), and north-eastern (0.4%) regions (see Figure 1). The eastern and north-eastern regions have a negligible share mainly due to the lack of availability of land for setting up solar projects and the heavy dependency on coal.

Figure 1: The distribution of solar capacity in different zones (source: CSTEP, data from CEA & MNRE)

India could become the largest solar power producer globally due to its abundant solar potential, ambitious solar targets of the government, and competitive auctions. Rating agencies forecast that the nation will add an additional 8.5 GW of solar capacity by 2022 as large-scale solar projects are in the pipeline. Market research companies anticipate the northern region to surpass the southern region in maximum installed solar capacity in 2022.

The Indian solar industry is slowly transitioning from polycrystalline to bifacial and mono-PERC solar module technologies because of their higher efficiency, longevity, and ability to reduce the balance of system costs. According to experts, bifacial panels and mono-PERC modules would soon gain huge traction in the domestic rooftop photovoltaic (RTPV) and utility-scale solar sectors, respectively. The cost of indigenously manufactured mono-PERC would be about INR 19.54–21.04/W and bifacial modules would be about INR 21.04–22.54/W, close to the price of conventional polycrystalline modules of around INR 18.78/W.

Utility-scale solar holds the largest share (84%) in the overall solar capacity of 48.56 GW, whereas the RTPV sector has mostly remained untapped. Unless the central and state governments make a coordinated effort, achieving RTPV goals would become challenging. An enabling policy framework is essential to bolster RTPV growth in 2022. The government could implement large-scale RTPV programmes under aggregator models—Capital Expenditure (CAPEX), Renewable Energy Service Company (RESCO), and Roof Rent—to offset the negative impact on distribution utility finances.

India has been looking at innovative ways to install solar capacity in agricultural lands, canals, and other water bodies. However, these new and innovative technologies—agrivoltaics, canal top PV, and floating PV—are at a nascent stage of development and have higher installation costs. Hence, the government needs to evaluate the technical potential, frame a consistent regulatory framework, create a domestic supply chain, and explore innovative business models to improve the cost-effectiveness of these technologies.

Eventually, with the rapid development of high performance and low-cost PV technologies, India could continue to play a leading role in the global solar revolution.

Jaymin Gajjar & Saptak Ghosh, Researchers at CSTEP

———————————

Discover more from SolarQuarter

Subscribe to get the latest posts sent to your email.

")

")

")

{kind=link}